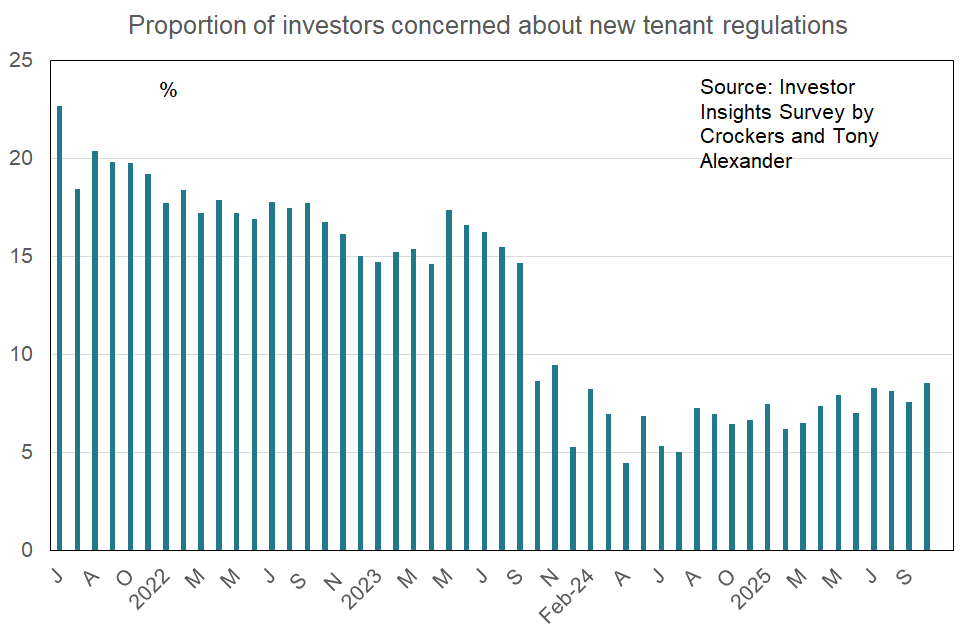

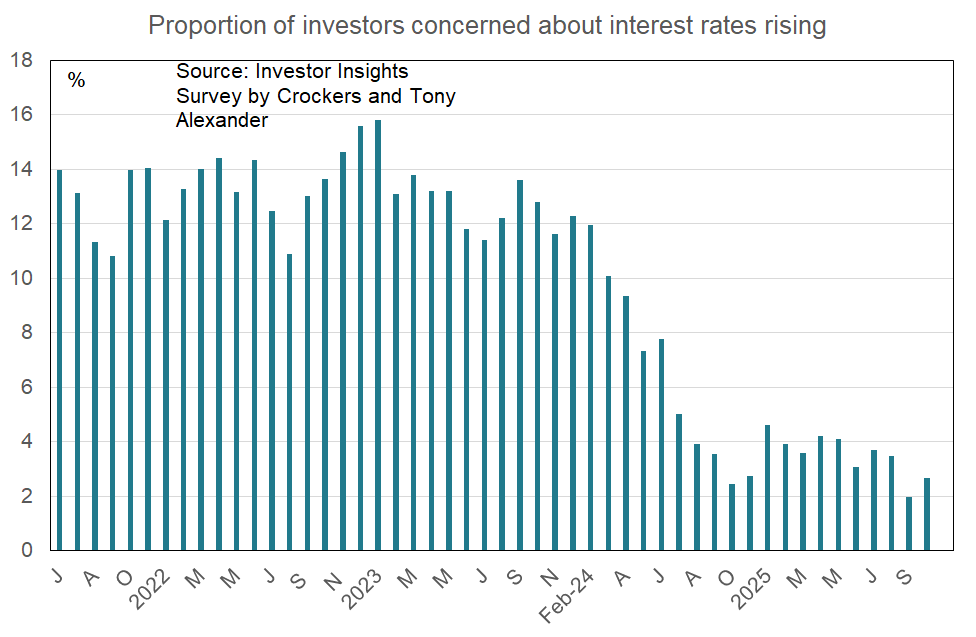

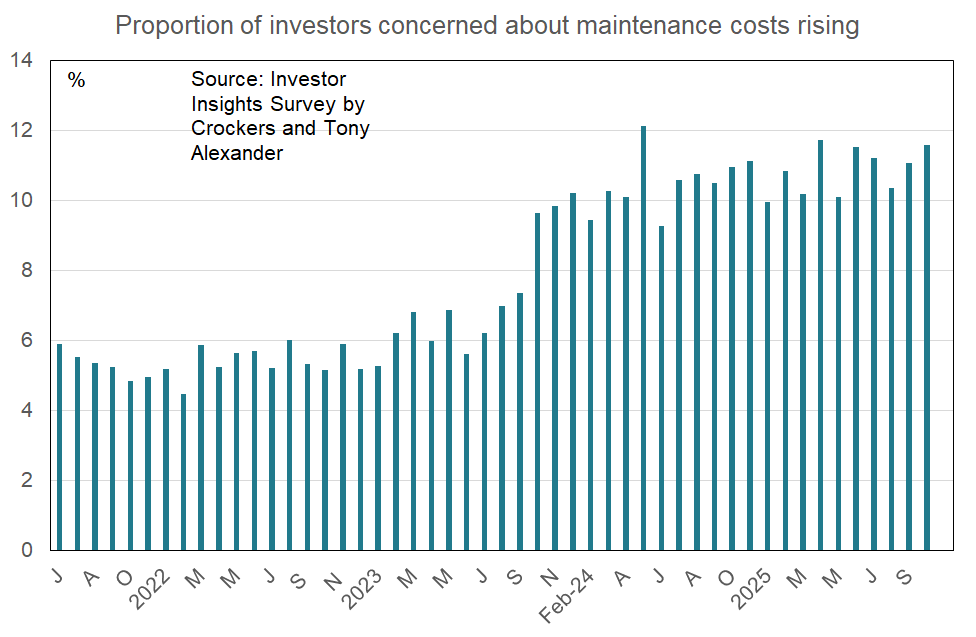

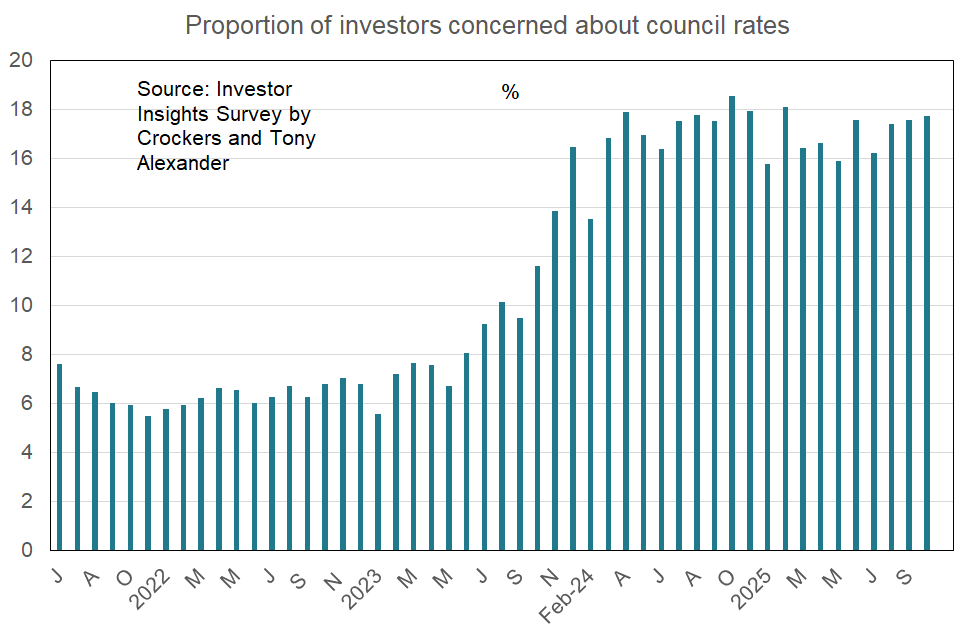

Higher interest in new builds

Welcome to the latest monthly Investor Insight survey compiled by Crockers Property Management and Tony Alexander. Each month we survey a selection of the many thousands of residential property investors on our databases with a view to gauging how things are changing over time across a wide range of indicators.

For instance, we will track changes in pressures on rents, points of particular concern, and plans regarding property purchases and intentions to sell.

Key points of interest from this month’s survey, which received 274 responses, include the following.

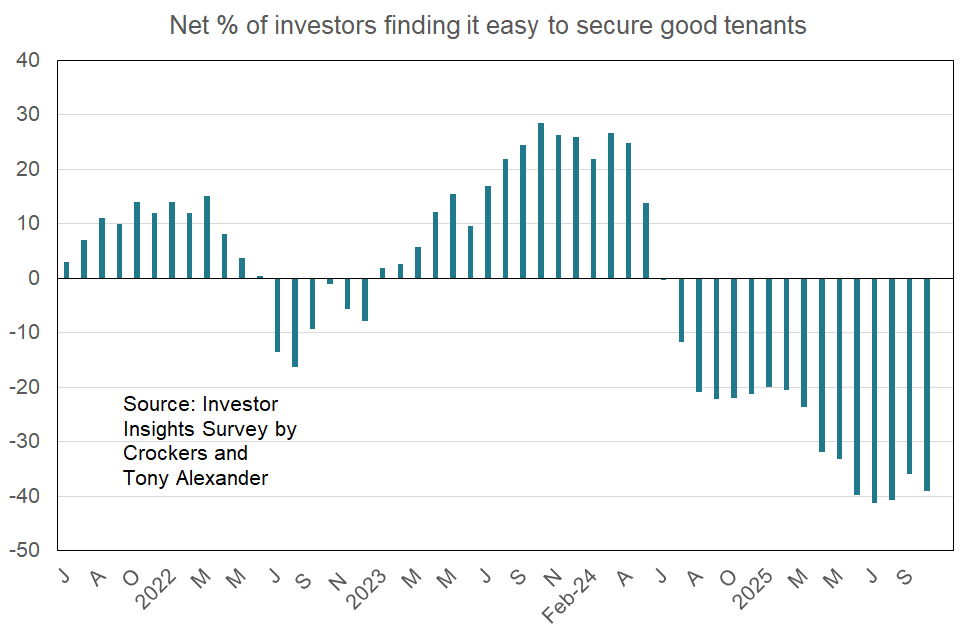

- A near record net proportion of landlords say that it is difficult to secure good tenants.

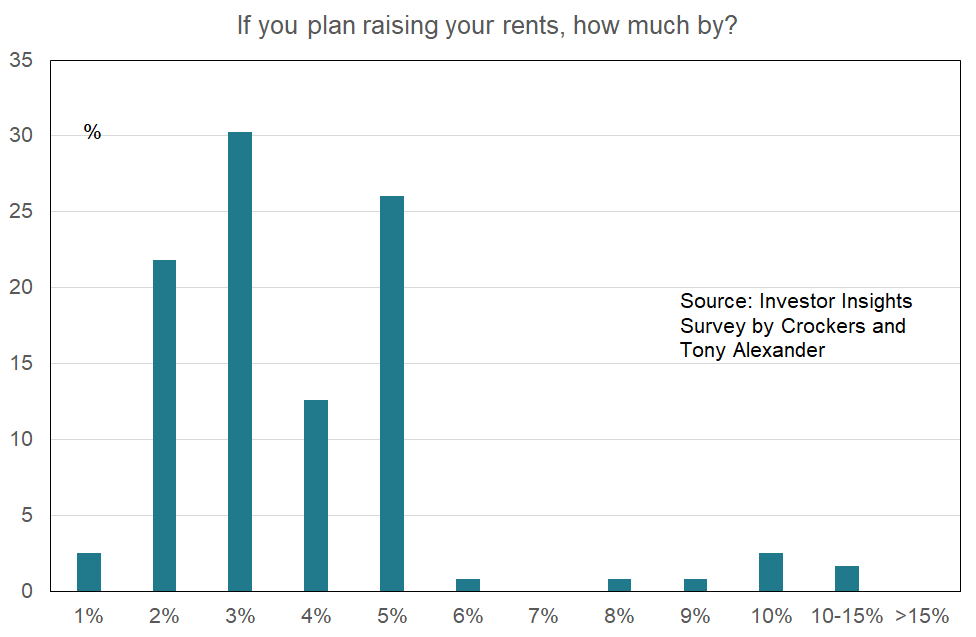

- The average amount by which property investors plan to raise rents in the coming year continues to slowly ease.

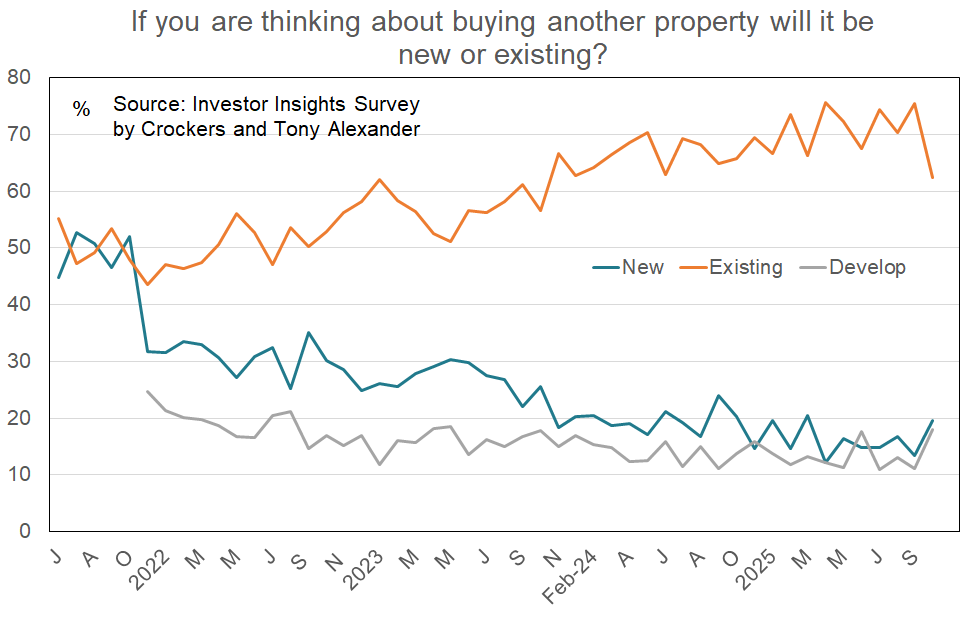

- For those looking to make a fresh purchase there has been a rise in interest in a new property.

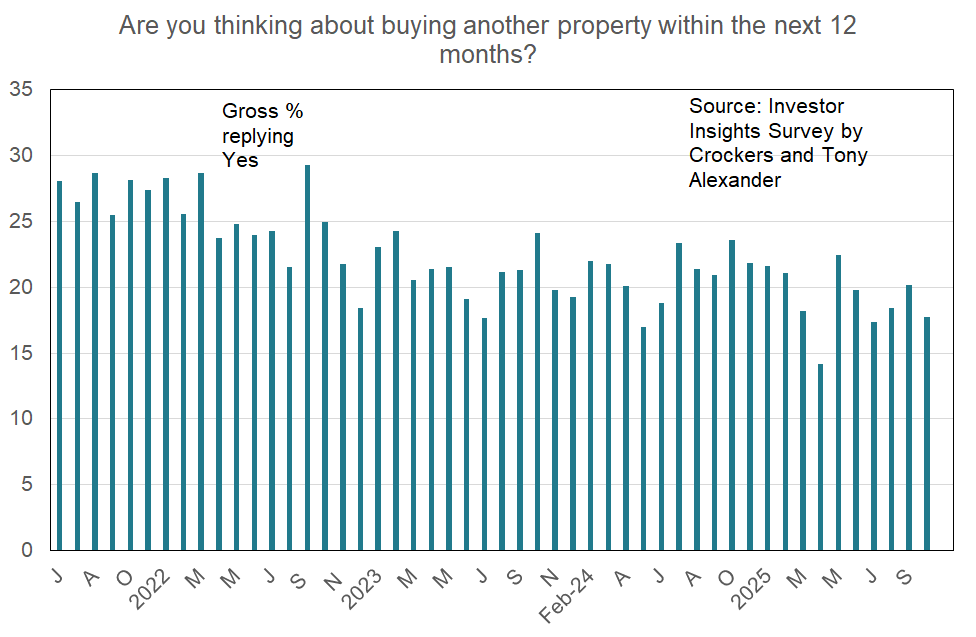

ARE YOU THINKING ABOUT BUYING ANOTHER PROPERTY WITHIN THE NEXT 12 MONTHS?

This month has brought a small decline in the proportion of existing landlords thinking about buying another property – down to 18% from 20% in September. This is where the level of interest was in August however, so there is no trend rise or decline underway in this important measure at the moment.

The main change in desire to buy happened throughout 2022 – as seen in the following graph when one looks beyond the monthly blips up and down.