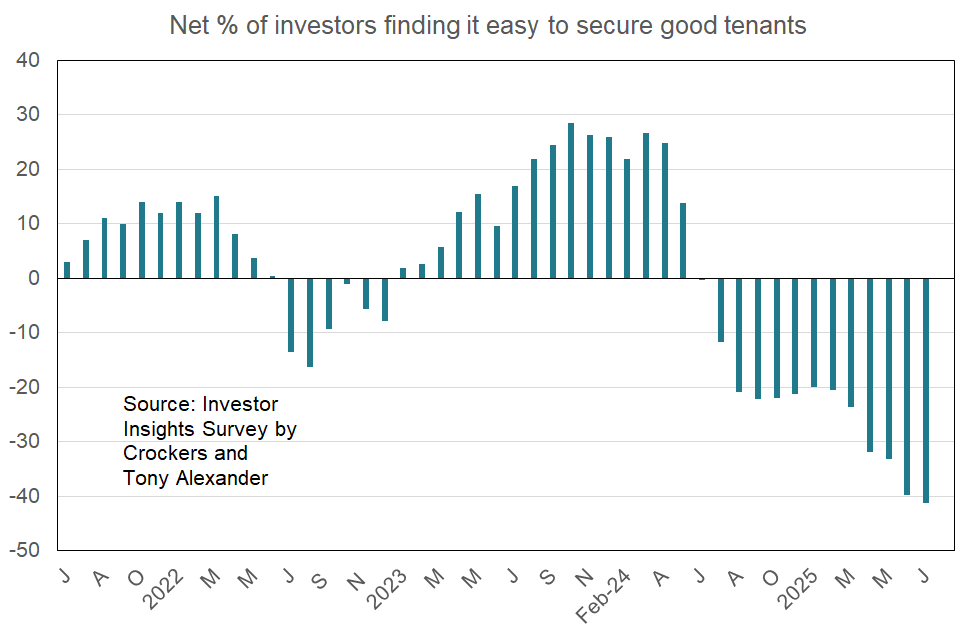

Tenant scarcity curbing rent rises

Welcome to the latest monthly Investor Insight survey compiled by Crockers Property Management and Tony Alexander. Each month we survey a selection of the many thousands of residential property investors on our databases with a view to gauging how things are changing over time across a wide range of indicators.

For instance, we will track changes in pressures on rents, points of particular concern, and plans regarding property purchases and intentions to sell.

Key points of interest from this month’s survey, which received 288 responses include the following.

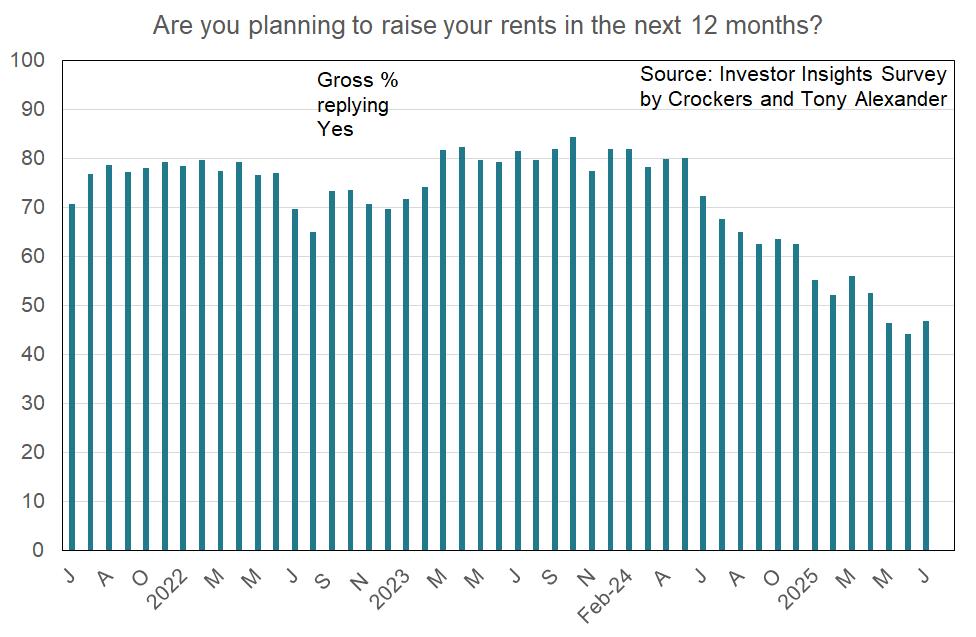

- Whereas 15 months ago a net 25% of landlords said that it was easy to find a good tenant, now a record net 41% say it is hard.

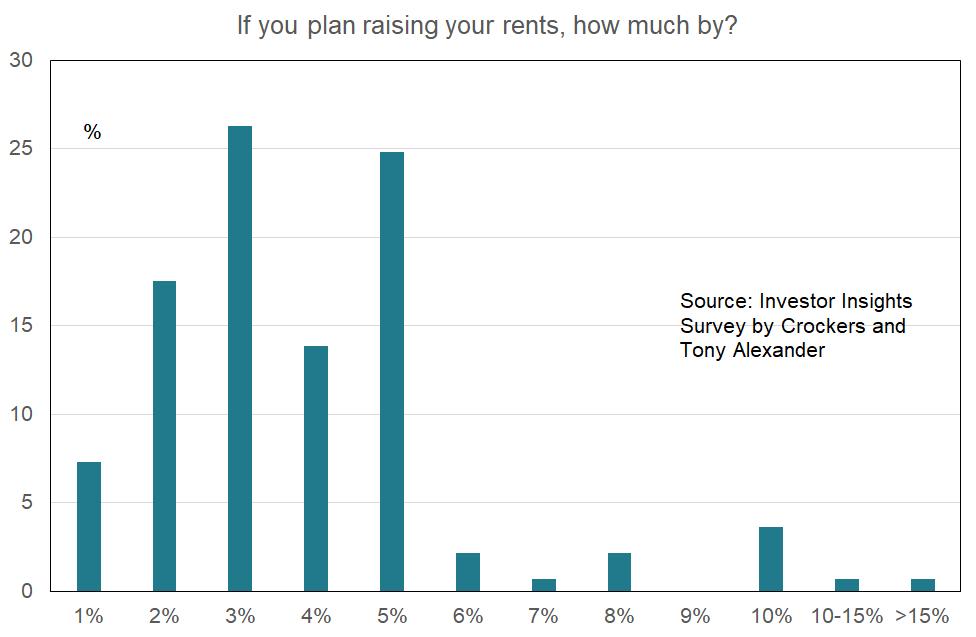

- Planned rent rises continue to slow down.

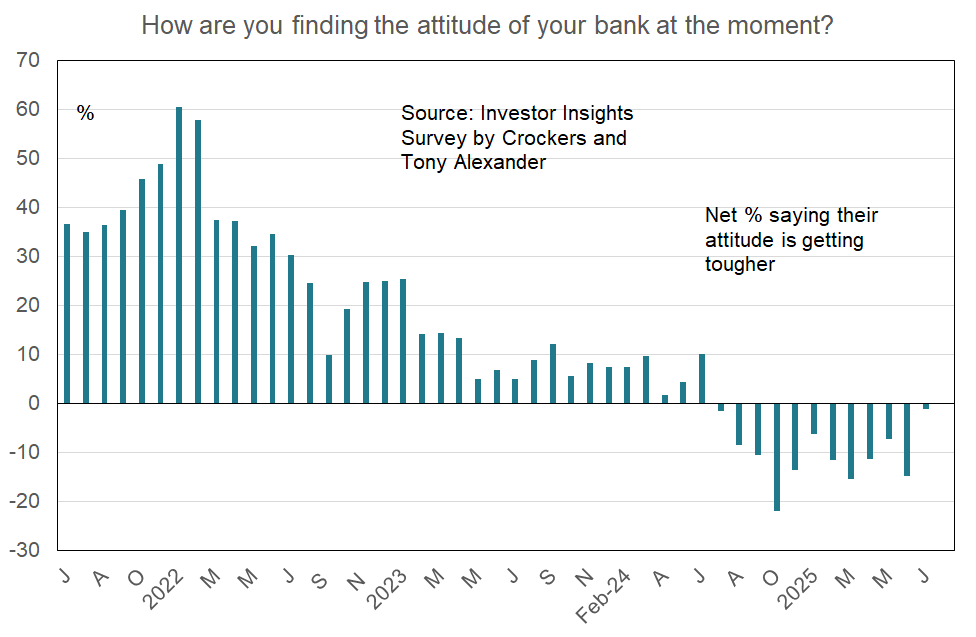

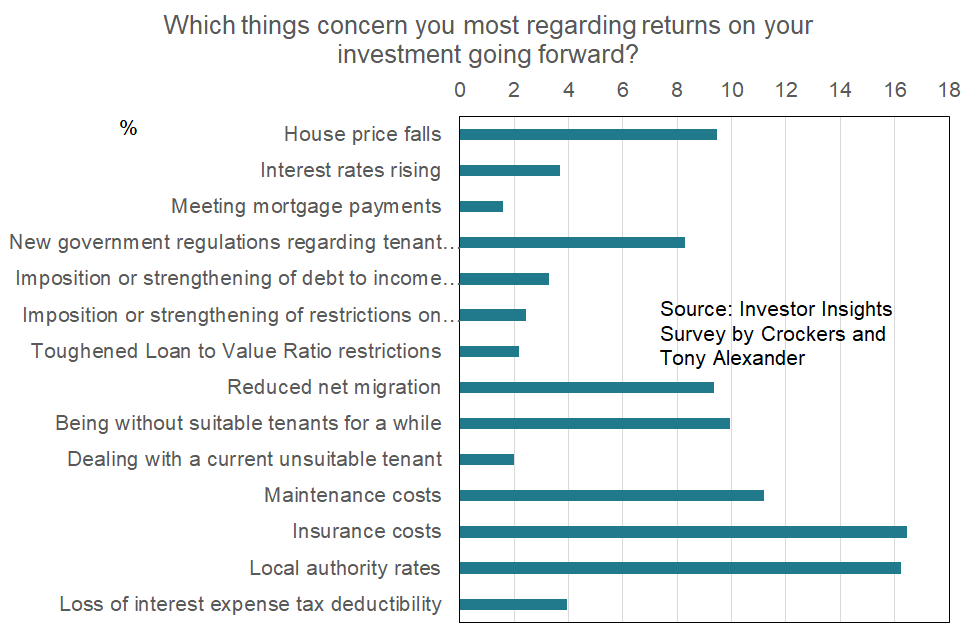

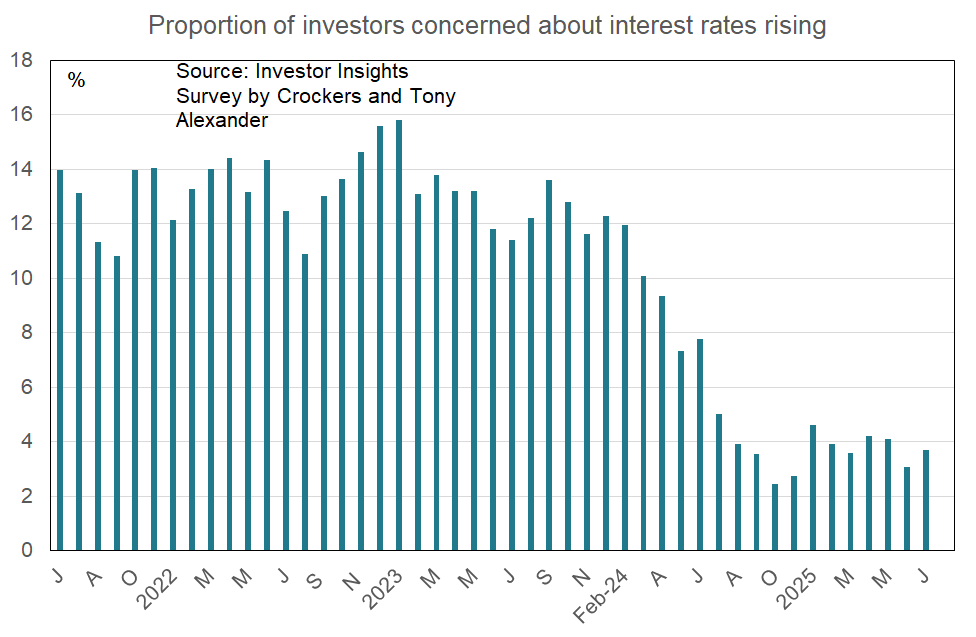

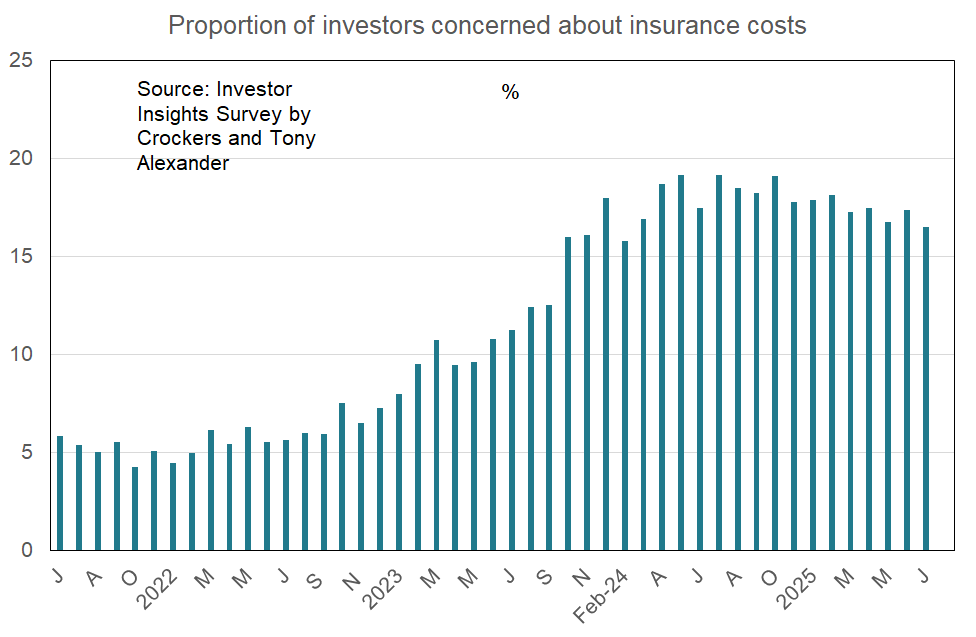

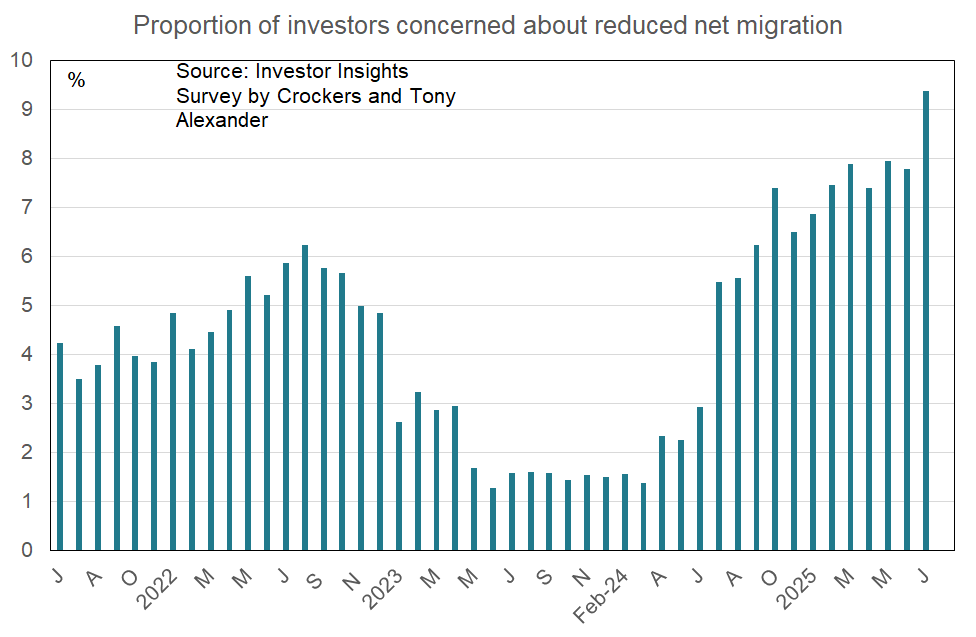

- Investors are slowly growing less worried about insurance premium increases but are becoming more concerned about weak migration flows.

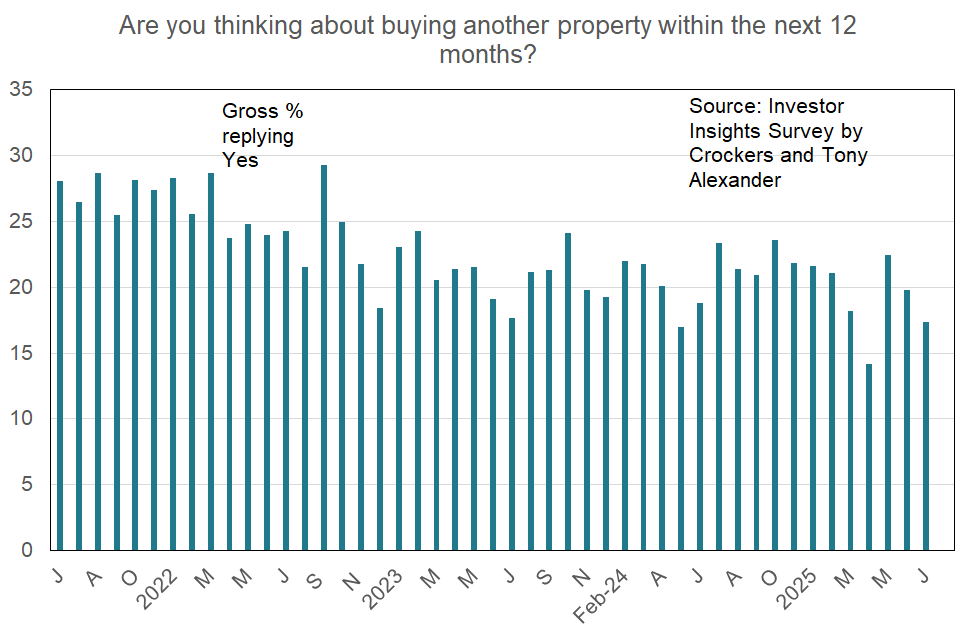

ARE YOU THINKING ABOUT BUYING ANOTHER PROPERTY WITHIN THE NEXT 12 MONTHS?

Only 17% of landlords reporting in this month’s survey have said that they are thinking about buying a property in the next three months. This is down from 20% in June and 22% in May and the graph hints that there may still be a downward trend in this gauge of investor demand. Note that declines have occurred during the period of falling interest rates from mid-2024.